Financial Independence/Early Retirement

06-30-2015, 04:04 PM

06-30-2015, 04:04 PM

#22

SADFab Destructive Testing Engineer

iTrader: (5)

Join Date: Apr 2014

Location: Beaverton, USA

Posts: 18,642

Total Cats: 1,866

While investing with your dad's friend is definitely preferable to putting it into a savings account I would still suggest you get an basic understanding of how he makes his money. Is he fee based or does he make money from the products he sells? You want someone who is fee based so that they have no incentive to sell you a product that provides them with high margins while providing you with less than optimal returns. <br />

<br /><br />

<br />To the traditional vs Roth question this is going to depend a bit on your situation. Mathematically, a traditional 401k or IRA will yield higher after tax returns due to the fact that most people fall into a higher income tax bracket while working than when they retire. However, Roth IRA's offer some additional flexibility before the age of 59 1/2 that might provide some value to you depending on your specific situation. If you have no interest in learning about finance for yourself this is definitely something I would discuss with a financial planner.

<br /><br />

<br />To the traditional vs Roth question this is going to depend a bit on your situation. Mathematically, a traditional 401k or IRA will yield higher after tax returns due to the fact that most people fall into a higher income tax bracket while working than when they retire. However, Roth IRA's offer some additional flexibility before the age of 59 1/2 that might provide some value to you depending on your specific situation. If you have no interest in learning about finance for yourself this is definitely something I would discuss with a financial planner.

<br /><br />

<br />The way my dad spoke about him is that he lays it all on the table for my dad. Tells him everything he can do, and the breaks it down into smaller decisions. I.e. high risk vs low risk. Do you want to invest in new tech or stable big companies. My dad pays some amount when buying stock and none when selling. He also has some money in managed funds. Where you put money in and then get a return based on the funds that are managed.

Reply

0

0

0

06-30-2015, 04:08 PM

#23

Senior Member

Join Date: Jan 2007

Location: Round Pond, ME

Posts: 1,064

Total Cats: 232

We own our house in CT outright, and have a small mortgage on our place in Maine. There are very legitimate arguments to be made that I should have big mortgages on both, but....

We are both 59, and only working because my wife actually likes her job, and I'm not sure what else to do yet. We can retire next week if we want - it gives you an entirely different perspective on a job to know you can tell your boss to **** off and walk.

All that money I could have spent on cars and restaurants and a McMansion went into 401k's, index funds, and a handful stocks that I have traded over

the last 25 years or so. I spent my 20's making(and losing) memories instead of money, so it was a later start than some.

I think putting the most possible into a 401k is probably the best/easiest way to start - consider that because it's pre-tax, your first-year return is equal to your marginal tax rate - 17%, 28%, higher - plus employer match plus whatever it grows. That's a hard rate to beat these days anywhere.

I have no advice on choosing other investments, because mine were the result of advice from a very astute FIL and good luck. Finding financial advice you can really trust is very tricky - clearly a job for MT.net! I got smart/lucky with a few stocks, and they allowed me to pay for the houses.

I like index funds(TIAA/CREF and Vanguard are 2 I've owned) because they generally do as well as or better than standard mutuals, and they have lower costs.

Reply

0

0

06-30-2015, 04:30 PM

#24

I have to say I really disagree with this. Starting your own business requires taking a huge risk and a certain level of business savvy to succeed. This is not a path for most and the chances of failure are quite high. If you do succeed the rewards can be quite large but it is far from the only or even best way to do it.

Retiring early has a lot more to do with being able to live off of less than you make. I posted the math above and it is really that simple. What you make doesn't matter. It just matters how much you can save. Making more means you can live on more while saving more and makes the process easier. However, If I can happily live off of 25% of my take home on $36,000 a year I would still be able to retire in 7 years if I planned to maintain the same standard of living adjusted for inflation for the rest of my life. The reason most people that retire early do it by running a small business is because they are able to sell the business and get a nice lump sum payment from their sweat equity that allows them to retire. Most people in the U.S. live near or beyond their means. Since most people don't have a business to sell that provides them a large windfall all at once they just never build up that nest egg over the course of their career.

Retiring early has a lot more to do with being able to live off of less than you make. I posted the math above and it is really that simple. What you make doesn't matter. It just matters how much you can save. Making more means you can live on more while saving more and makes the process easier. However, If I can happily live off of 25% of my take home on $36,000 a year I would still be able to retire in 7 years if I planned to maintain the same standard of living adjusted for inflation for the rest of my life. The reason most people that retire early do it by running a small business is because they are able to sell the business and get a nice lump sum payment from their sweat equity that allows them to retire. Most people in the U.S. live near or beyond their means. Since most people don't have a business to sell that provides them a large windfall all at once they just never build up that nest egg over the course of their career.

Based on your math, everyone should be retired at 40. And in reality, life happens and a large percentage of the population don't retire before 40. Thus while your math makes sense, and is right, and I agree with it too, reality is it too is doesn't have a high success rate. Though it has potential.

Anyways my goals for retirement are different than yours, thus my approach is different. I could not work for someone else and reach my retirement goals. I tried to actually, and it wasn't working.

Reply

0

0

06-30-2015, 05:39 PM

06-30-2015, 05:39 PM

#26

Elite Member

Thread Starter

iTrader: (8)

Join Date: Jan 2012

Location: Tampa, Florida

Posts: 2,568

Total Cats: 217

Unless you choose to sell the house in California when you retire and move to a lower cost of living area. As long as the home maintains or builds value it can be a good investment. If you, however, plan to live in it forever than that is an entirely different story.

Reply

0

0

06-30-2015, 06:26 PM

#27

SADFab Destructive Testing Engineer

iTrader: (5)

Join Date: Apr 2014

Location: Beaverton, USA

Posts: 18,642

Total Cats: 1,866

<p>Just spent half an hour on the phone with the meryl lynch guy. First we talked about what kind of IRA to put money in and I think a Roth IRA is the way to go. Althought my tax rates might go up, if I retire, or start making less money. Or tax rates in general skyrocket (very possible) then I will be happy I put it in.</p><p>Then in a few months after a couple pay checks and helping the savings. Look at my monthly spending, decide how much I should keep in savings for emergencies, and start putting the rest of my paycheck in some sort of investment. He suggested mutual funds to start with.</p>

Reply

0

0

06-30-2015, 06:48 PM

#28

Moderator

iTrader: (12)

Join Date: Nov 2008

Location: Tampa, Florida

Posts: 20,645

Total Cats: 3,009

I think I found my easy button. Just called my dad and he has an old college friend who is at Meryl lynch and manages all of his investments. He has a son who is also about to take up the business. My dad said that he trusts him with his money and all he has to do is talk to him every few months and discuss some investment ideas. I'm going to get in contact with him. I think by staying with someone who knows my family I can find a way to do it. I'll report back when I meet with then.

Roth 401k or normal?

Roth 401k or normal?

And expense ratio is a number with a decimal point in it. It is a multiplier. However much money you have in the fund is multiplied by the expense ratio and that is how much money the bankers take from you each year. They take it even if they screwed up and you lost money with the investment they chose for you.

The management fee is another fee that is similarly multiplied and deducted.

Ok, Merrill Lynch (owned by Bank of America) has funds on their website to chose from with a expense ratio (just picking one that looks like the middle of the range) of 1.270. Vanguard Small Cap Index fund has an expense ratio of .09. So, let's say you have $10K in each fund. Merrill takes $127 and Vanguard takes $9. You see why Merrill guy has a nice car and a country club membership? Vanguard is investor owned so they keep costs down. As Ryan was saying, you don't need suit-and-tie guy to shake your hand and tell you how smart you are to let him help you. Ryan is saying "index funds" simply because they are safe, easy, and the expenses are low.

Really quickly, small cap, mid cap, large cap just refer to the size of the various companies on the stock market. General Electric is large cap. Cummins Engines is a small cap. Cap is short for capitalization, or money. There are many more small cap companies than large cap. More terminology: index funds, just like an index lists everything covered in a book, an index of stock market funds is just one of everything. Therefore a small cap index fund is a fund that has a little piece of all of the small companies on the stock market. That includes everything from engine manufacturers to biomedical companies, restaurants to homebuilders, aerospace to Abercrombie.

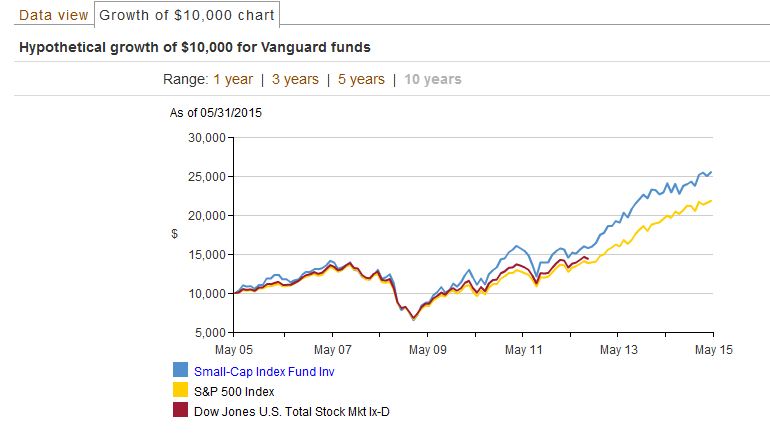

The last time I checked, the Vanguard's Small Cap Index Fund had just under 1500 companies in it from all types of companies so you are automatically diversified, spread out for your own protection. And, if you think logically about it, a small company has a much greater chance of growing by 10% in a year than a very large company, and many do. Small cap index funds typically outperform the stock market average or S&P500 by a large gap. Another really nice thing about an index fund is that it doesn't require much fund management (deciding which funds to include) so the expense ratio is usually quite low.

The way my dad spoke about him is that he lays it all on the table for my dad. Tells him everything he can do, and the breaks it down into smaller decisions. I.e. high risk vs low risk. Do you want to invest in new tech or stable big companies. My dad pays some amount when buying stock and none when selling. He also has some money in managed funds. Where you put money in and then get a return based on the funds that are managed.

Small cap index funds don't require you being concerned with high or low risk. They are safe, cheap, and will make you money over time without worry.

I'm not quite on Ryan's plan (anybody want to buy a lake house?) when it comes to austerity, but I buy used vehicles with cash and have nearly paid off my small primary house.

Reply

0

0

06-30-2015, 06:53 PM

#29

Moderator

iTrader: (12)

Join Date: Nov 2008

Location: Tampa, Florida

Posts: 20,645

Total Cats: 3,009

You can open an IRA or just simply buy mutual funds without any help by just going on Vanguard.com and opening up an account. It really is very easy.

Here is the list of funds in the Vanguard Small Cap Index Fund, which is pretty interesting to look through: https://personal.vanguard.com/us/Fun...sortOrder=desc

Here is the list of funds in the Vanguard Small Cap Index Fund, which is pretty interesting to look through: https://personal.vanguard.com/us/Fun...sortOrder=desc

Reply

0

0

06-30-2015, 06:56 PM

#30

I've been sitting on a modest 5 figure bank account for the last decade accumated from rent income, and holy cow I finally got around to seeing how I can grow it.. I cant belive how much more I could have with a few decent investments... Shoved half of it into a few vanguard funds. Been about a month so far and the markets have been rough, lost about $80 So far. Not ready to jump into stocks yet.

I wasn't really raised with an investment mentality.. The most anyone in my family has ever done was CDs, big banks are all they know. I'll be breaking that cycle.

I wasn't really raised with an investment mentality.. The most anyone in my family has ever done was CDs, big banks are all they know. I'll be breaking that cycle.

Reply

0

0

06-30-2015, 07:02 PM

#31

Vanguard Index Funds are fantastic. Look for well balanced index funds with low fees. The lower the fee, the better. Unless you make it your full time job, you're not going to time the market swings correctly, and even the guys doing it for a full time job screw it up more often than not.

I will throw a little bit of caution on going too heavy on the small cap index, though. The last 5-10 years has been historically out of the norm in small cap performance, so when you look at index performance it looks like small cap is the best deal. That doesn't mean that it will be true over the next 5-10 years, however. If you expand the history out to 30 or 40 years, then you'll see more of a balance between small cap, med cap, and large cap funds.

I will throw a little bit of caution on going too heavy on the small cap index, though. The last 5-10 years has been historically out of the norm in small cap performance, so when you look at index performance it looks like small cap is the best deal. That doesn't mean that it will be true over the next 5-10 years, however. If you expand the history out to 30 or 40 years, then you'll see more of a balance between small cap, med cap, and large cap funds.

Reply

0

0

06-30-2015, 07:03 PM

#32

Moderator

iTrader: (12)

Join Date: Nov 2008

Location: Tampa, Florida

Posts: 20,645

Total Cats: 3,009

I've been sitting on a modest 5 figure bank account for the last decade accumated from rent income, and holy cow I finally got around to seeing how I can grow it.. I cant belive how much more I could have with a few decent investments... Shoved half of it into a few vanguard funds. Been about a month so far and the markets have been rough, lost about $80 So far. Not ready to jump into stocks yet.

Individual stocks are for the very well educated with lots of time to devote to a second job of market watching.

Reply

0

0

06-30-2015, 07:20 PM

#36

<p>

</p><p> </p><p>Thats where I'm at too. Retirement savings is max out 401k that employer will at least partially match, max out max roth 401k contribution. Any exccess disposible income goes into a mutual fund which is my emergency fund and savings for a down payment on a house. </p><p> </p><p>Well, minus the miata investment which has the best return of investment of all options. Miata is on average rate of return of 15% of my happiness. </p>

</p><p>Just spent half an hour on the phone with the meryl lynch guy. First we talked about what kind of IRA to put money in and I think a Roth IRA is the way to go. Althought my tax rates might go up, if I retire, or start making less money. Or tax rates in general skyrocket (very possible) then I will be happy I put it in.</p><p>Then in a few months after a couple pay checks and helping the savings. Look at my monthly spending, decide how much I should keep in savings for emergencies, and start putting the rest of my paycheck in some sort of investment. He suggested mutual funds to start with.</p><p>

Reply

0

0

06-30-2015, 07:33 PM

06-30-2015, 07:33 PM

#38

Moderator

iTrader: (12)

Join Date: Nov 2008

Location: Tampa, Florida

Posts: 20,645

Total Cats: 3,009

Matching is awesome. Use that. It is free, automatic growth on top of everything else you will make. Put all you can into it. Just choose wisely with regard to expense ratios when choosing which fund(s) within your company 401k to invest in. The company will have a list of funds to choose from. Some will be more expensive than others. If you provide a copy of that list, I would be happy to take a look at the funds and tell you a little about the choices. It is tough to navigate when starting out.

Reply

0

0

06-30-2015, 08:01 PM

#39

The long term average is what you want to keep your eye on. If you are looking to park money for a few months, use a bank. If you are interested in 10%+ growth over the long haul instead of losing money in a savings account at .03%, then you are ready. The whole stock market average since 1965 is about 10% growth per year. The small cap index will usually significantly outperform that.

Individual stocks are for the very well educated with lots of time to devote to a second job of market watching.

Individual stocks are for the very well educated with lots of time to devote to a second job of market watching.

Reply

0

0

06-30-2015, 09:19 PM

#40

SADFab Destructive Testing Engineer

iTrader: (5)

Join Date: Apr 2014

Location: Beaverton, USA

Posts: 18,642

Total Cats: 1,866

<p>

</p><p>Thanks 6. I have to wait for like a week or so to get added to the financial benefits system. I'll shoot you a PM then.</p>

Matching is awesome. Use that. It is free, automatic growth on top of everything else you will make. Put all you can into it. Just choose wisely with regard to expense ratios when choosing which fund(s) within your company 401k to invest in. The company will have a list of funds to choose from. Some will be more expensive than others. If you provide a copy of that list, I would be happy to take a look at the funds and tell you a little about the choices. It is tough to navigate when starting out.

Reply

0

0