CC rate increases

Thread Starter

I EAT CUM

iTrader: (6)

Joined: Sep 2008

Posts: 1,198

Total Cats: 0

From: Redneck, Texas

This **** is really starting to **** me off! Anybody else dealing with this variable rate bullshit with their card company? I had 10% interest with WellsFargo and they shoot me up to 15%. CITI went up to 23%! WTF is with these people? I owe practically nothing on them but still! So I decided to consolidate my small debts onto my Chase card which has been at 6.24 for the last...what...3 years? Now.....they are changing it to 13.24%! ******* bullshit. Now I'm stuck with what I should do next. After talking with Chase, it appears you can close your account now and keep making payments on your debt at the current interest rate until your debt is paid off. So the question is...close that account and start another one with a promotional offer? Or just keep it closed and stop using cc's period?

Reply

0

0

0

If you have no credit cards and are not paying a mortgage or anything. Then its hard to maintain credit. Its best to just have a card and keep the balance low to none on a revolving basis. That shows companies that if they lend you money they will get it back. If you cancel all your cards then when they pull your credit history they will see that you have none, and your rate will be higher.

Reply

0

0

Me and the wife have 1k limits on our cards. We only have 3. Only use 2, 3rd is for emergencies only. Usually never put more than 300-600 on them. When we do we usually pay it off within a few weeks. Haven't been charged interest or any fee's yet. We also have a mortgage. All cars bought for cash. I try not to owe people money aside from mortgage. That way I don't get in trouble. Last time we checked scores both were over 760. I think that's pretty good.

Reply

0

0

just pay it off sooner. I know all about college cc debt. It blows dick. The rate on the citicard I have from college is at like 29% or some ridiculous highway robbery number. Its PIF and I just use it every month to pay for gas. I also pay it off every month. So I never pay 29% on it and I still build my credit.

Reply

0

0

I'd say thats a great score, excellent actually. CCs are a good thing to have if you can be responsible with them. As a young man, like myself, they will help me build my score so when it comes time for me to buy a house I can actually get that low rate that they advertise and not something a couple points higher.

Reply

0

0

I've paid my way out of a $12k cc debt once in this lifetime...never again. That was at 20..I learned.

One credit card between us...paid in full every two weeks. Super low interest...and we threaten to cancel every time they threaten to raise it.

One credit card between us...paid in full every two weeks. Super low interest...and we threaten to cancel every time they threaten to raise it.

Reply

0

0

Reply

0

0

), but pay every penny back at the end of the month. If I can't afford it, it doesn't go on the card...

), but pay every penny back at the end of the month. If I can't afford it, it doesn't go on the card...

Reply

0

0

I'm Miserable!

iTrader: (16)

Joined: Dec 2008

Posts: 1,296

Total Cats: 0

From: where most people are Utarded

I learned the hard way a long time ago with credit cards. Ran my credit through my new credit union last week and I am only 7 points away from paying ZERO closing costs when I buy a house in the near future. They are also offering me a revolving line of credit at 5% fixed interest that will likely bump my score up another 15 points or so. I have paid cash for all 4 Miatas and every part I put on them, and have no sympathy for credit card racers.

Your credit card companies are likely trying to make as much as they can before they are regulated at the beginning of the new year.

Your credit card companies are likely trying to make as much as they can before they are regulated at the beginning of the new year.

Reply

0

0

Joined: Sep 2005

Posts: 34,429

Total Cats: 7,548

From: Chicago. (The less-murder part.)

I have one credit card. I have always had one credit card. It's quite likely that I will continue to always have one credit card, or whatever equivalent technology supersedes it. (Employer-issued corporate cards don't count.)

For the majority of day-to-day stuff (gas, groceries, restaurants, personal lubricant, etc) I use my debit card. I do this primarily because so long as I make 12 or more transactions per month, I get a 4.5% APY from my credit union on my checking account balance. (You could actually make money by getting a HELOC and depositing it. I wonder if anybody has actually done this?)

For things like internet or phone-based transactions, I use the credit card. This is principally because credit card companies provide a relatively high level of protection from fraud in the form of limited liability. You don't get that from a debit card, even if it says "Visa" on the front. I also use it for certain applications where a credit card is required, such as car rentals. As it happens, my card issuer also provides me with complimentary car rental and travel insurance.

About once a month or so I try to remember to log on and zero my CC balance. They really do make it quite easy, just key in a transfer from the checking account and hit "OK".

I don't think I've ever looked at what my rate is until today. It's Prime + 3.9%, minimum 9.99%, maximum 19.99%. So it's 9.99% now, which is the same as it's been for a while. (The prime rate hasn't been over 6.09% since Jan, 2008).

But it doesn't matter, since I've never paid it.

Before you nay-sayers tell me "By never carrying a balance, you're not establishing credit" you need to read up on how the rating companies work.

Short version: It is the ratio of credit used to available credit that matters.

In other words, let's say that I have a credit limit of $50,000, and on average, I have a balance of $1,000. (This doesn't mean that I carry that $1,000 balance across a full month and thus pay interest on it, merely that over a 30 day period, the average balance was $1,000.) I am using 2% of my available credit. This is considered a good thing, because it means that I don't tend to overspend. Thus, a lender can happily give me a loan to buy another boat and be reasonably certain that I will be able to pay it off. (Not that I'd take out a loan for something like that. Cash is king when it comes to luxury goods.)

But what if my credit limit is only $1,500 and yet I have the same average balance of $1,000? That would be a bad thing. I'd be using 66% of my available credit, and this indicates that I do tend to overspend relative to my ability to pay. I am thus a high-risk borrower, so no boat for me. A canoe, maybe.

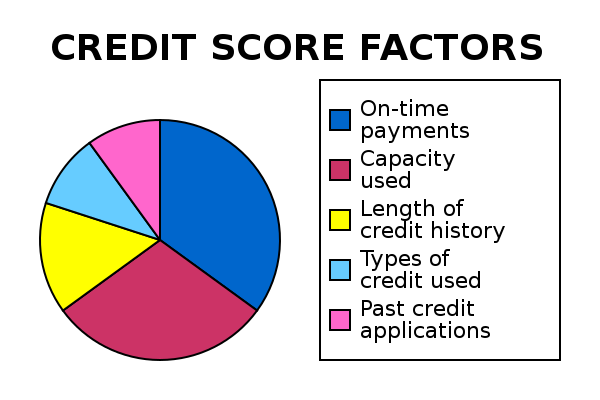

Credit utilization (that which we have discussed above) accounts for 30% of your credit score. Payment history (including mundane things like your phone bill) count for 35%. In other words, being a chronic late-payer of bills is worse than having ten credit cards all maxed out and making minimum payments. The rest is length of history (basically, your age), diversity of credit products previously utilized, and number of recent inquiries. (Applying for credit hurts your credit. Gotta love that one.)

Last time I checked (which was a year or so ago) my credit score was somewhere in the high 700s. This, despite the fact that I haven't made a car payment since ~2002, or a mortgage payment since 2004.

I'm glad that we could have this little chat. Shalom.

Last edited by Joe Perez; Oct 28, 2009 at 12:14 AM. Reason: Schpelling

Reply

0

0

Joined: Sep 2005

Posts: 34,429

Total Cats: 7,548

From: Chicago. (The less-murder part.)

Personally, I think the new regs suck. The CC companies not being able to rape stupid people means that they're probably going to have to cut back on some of the perks that responsible card users are afforded.

Reply

0

0

To be completely honest I never knew that using say, 60% of your total allowed credit makes you an "overspender". Guess I'll have to raise my credit card limit so that I'm at 30% or lower. Thanx JOe

Reply

0

0

Joined: Sep 2005

Posts: 34,429

Total Cats: 7,548

From: Chicago. (The less-murder part.)

The idea was to illustrate the general concept, not to provide specific guidelines. But you're correct in that, all else being equal, raising your credit card's limit will improve your credit utilization ratio, assuming that you spending habits remain consistent.

Now that I think about it, I probably should do this. When I signed up for my current card, I requested a $10k limit, which was the lowest available for that class. Normally I don't go anywhere near that, but now that I'm freelancing, these NYC hotel bills are probably making me look bad...

Reply

0

0

When I was working in NYC for work, I would stay across the river on the NJ side of the Lincoln Tunnel in Secaucus. There is a Hampton Inn there that is pretty nice and only runs like $120/night. If you are staying in Manhattan you are getting raped. Even if you are being reimbursed, its hard to have those bills sitting on your card while you wait for a check.

Reply

0

0

Joined: Sep 2005

Posts: 34,429

Total Cats: 7,548

From: Chicago. (The less-murder part.)

Yeah, I know there's a bunch of stuff over there, but PATH can suck my ***. When I'm in town for a month or two at a time, I really don't want to have to deal with the commute every day, especially since I do occasionally get emergency calls in the middle of the night. Much easier if I'm in midtown near the 1/2/3 line, or in SoHo / the village, within walking distance.

I just need to be more disciplined about transferring funds to the card as soon as each big charge hits, rather than waiting until three or four of them have stacked up. I just logged in a while ago (while checking the rate for the previous post) and saw that there was $6k on the tab since Oct 1. Zeroed it.

(That's not all hotel, of course. A couple of airplane tickets, a rental car here in CA, and a couple of computers were on there too.)

I just need to be more disciplined about transferring funds to the card as soon as each big charge hits, rather than waiting until three or four of them have stacked up. I just logged in a while ago (while checking the rate for the previous post) and saw that there was $6k on the tab since Oct 1. Zeroed it.

(That's not all hotel, of course. A couple of airplane tickets, a rental car here in CA, and a couple of computers were on there too.)

Reply

0

0

I guess if you are worried about the commute then that kills it for you. For most of the day the Lincoln Tunnel is a quick minute crossing. Even at like 3pm I was able to go from my hotel in Secaucus to the Verizon Wireless across the street from Bryant Park in like 15min.

Reply

0

0